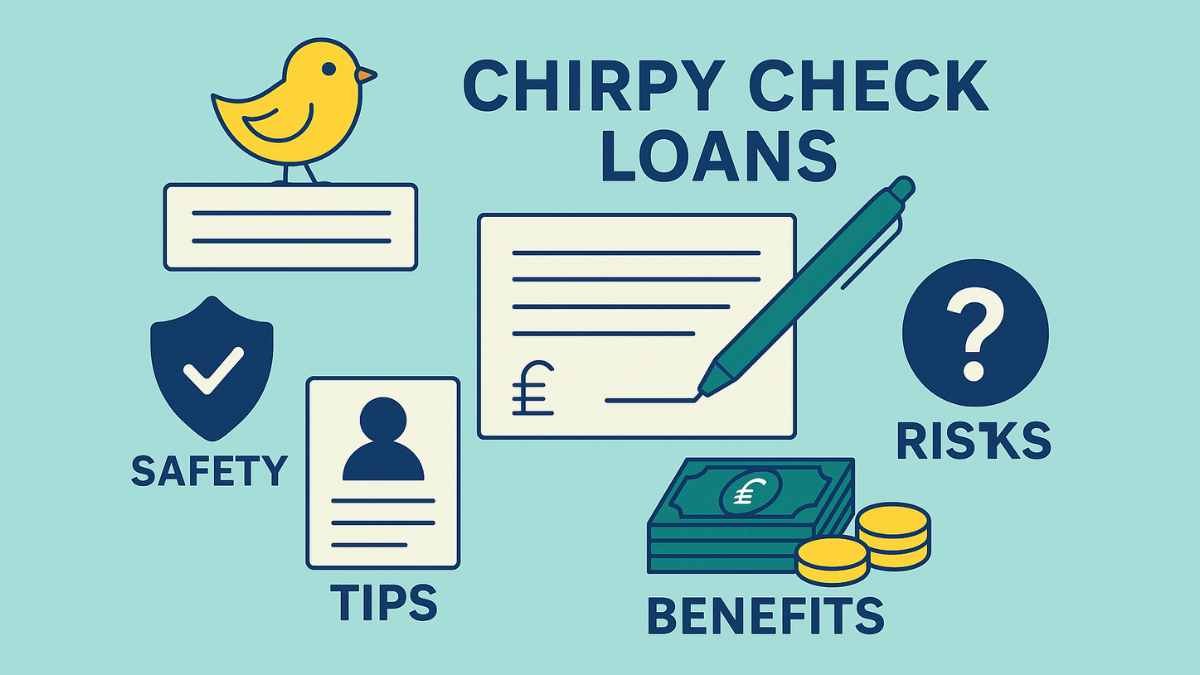

Chirpy Check Loans: A Complete Guide to Understanding Services, Safety, and Customer Expectations

The financial landscape has transformed dramatically over the past decade, giving rise to new lending platforms, digital loan services, and alternative credit solutions aimed at simplifying access to short-term finance. Among the growing list of financial terms people search for today is “chirpy check loans”, a phrase that has gained attention as consumers look for quick, convenient, and straightforward lending options. Yet, despite its increasing popularity in online searches, there remains confusion regarding what exactly chirpy check loans are, how they work, and whether they can be trusted.

What Are Chirpy Check Loans?

The term chirpy check loans is not tied to a widely recognised, mainstream financial institution. Instead, it appears to describe a type of short-term loan service often associated with quick applications, minimal credit verification, and simplified approval processes. These loans typically appeal to individuals who need fast cash for emergencies, personal expenses, or unexpected bills.

While the exact branding “chirpy check loans” may be used by smaller or emerging lenders, the concept aligns with what is commonly known as “quick-check loans” or “instant-decision loans”. These are loans where the approval process is significantly faster than traditional bank credit checks, relying on streamlined assessments or alternative methods of verifying income and identity.

How Chirpy Check Loans Typically Work

Although chirpy check loans are not tied to one clearly established provider, their general framework tends to follow common lending patterns:

1. Simple Application Process

Most platforms using this structure aim for minimal effort from the borrower. Applications are usually completed online, requiring basic personal information, employment status, and proof of income.

2. Fast Approval Times

The defining characteristic is rapid decision-making. Many quick-check lenders claim to offer approval within minutes, using automated systems to assess eligibility.

3. Short-Term Repayment Structure

Chirpy check loans usually fall under short-term borrowing, meaning repayment is expected within a few weeks or months rather than years. This makes them appealing for temporary financial challenges.

4. Small to Moderate Loan Amounts

These loans commonly range from small sums suitable for unexpected expenses to moderate amounts for urgent needs. They are not typically used for long-term financial planning.

5. Higher-Than-Average Interest Rates

Due to their speed and accessibility, interest rates on chirpy check loans may be higher compared to traditional bank loans. This helps lenders manage risk when offering credit to borrowers with limited financial history.

Why People Search for Chirpy Check Loans

There are several reasons why this keyword has been appearing frequently in online search trends:

1. Need for Emergency Funds

Many individuals experience sudden financial stress—medical bills, vehicle repairs, home emergencies—and seek quick solutions.

2. Difficulty Securing Traditional Loans

Borrowers with limited credit history or low credit scores may turn to alternative loan services advertised as easy-approval options.

3. Digital Convenience

Modern consumers prefer services that operate online, without the need for in-person appointments or lengthy paperwork.

4. Curiosity About New Loan Brands

When new or unfamiliar loan providers appear online, people often search their names to check legitimacy before applying.

Benefits of Chirpy Check Loans

While not without risks, chirpy check loans may offer several advantages when used responsibly:

1. Fast Access to Money

The ability to receive funds promptly can be invaluable during emergencies or time-sensitive situations.

2. Straightforward Requirements

Traditional lenders may require extensive financial documentation, whereas quick-check services typically request only the essentials.

3. Inclusive Eligibility Criteria

These lenders often consider borrowers who may otherwise struggle to secure financing through conventional banks.

4. Fully Digital Process

Applications, approvals, and fund transfers are usually completed online, offering ease and convenience.

Risks and Concerns Associated with Chirpy Check Loans

It’s crucial to be aware of the potential downsides before seeking a chirpy check loan.

1. Lack of Verified Information

Because the term is not tied to a well-known financial institution, borrowers must exercise caution. Unregistered or unregulated lenders pose significant risks.

2. High Interest and Fees

Convenience comes at a cost. Higher interest rates may make repayment challenging for some individuals, leading to debt cycles.

3. Potential for Fraud or Misrepresentation

Unfamiliar loan names can sometimes be associated with scams. Borrowers must ensure that the lender is legitimate before sharing personal or financial information.

4. Impact on Financial Stability

Short-term loans, if misused, can strain monthly budgets, particularly when repayment deadlines are tight.

How to Identify a Legitimate Chirpy Check Loan Provider

If you encounter a lender claiming to offer chirpy check loans, follow these essential verification steps:

1. Check Regulatory Registration

Any credible loan provider must be registered with the relevant financial authority in your region. For example, UK lenders must be authorised by the Financial Conduct Authority (FCA).

2. Review Customer Feedback

Search for reviews, complaints, and experiences shared by other borrowers. Lack of online presence is a major red flag.

3. Confirm Physical Address and Contact Information

Legitimate companies provide verifiable addresses, phone numbers, and customer service channels.

4. Read Terms and Conditions Carefully

Before applying, ensure you understand interest rates, fees, repayment periods, and late payment penalties.

5. Avoid Upfront Payment Requests

No genuine loan provider should ask for fees before providing the actual service.

Alternatives to Chirpy Check Loans

If you are uncertain about unfamiliar lenders, several safer alternatives exist:

1. Credit Unions

Often offer lower interest rates and flexible repayment options.

2. Bank Overdraft Facilities

These may provide immediate funds depending on your account standing.

3. Salary Advances

Some employers offer emergency advances to help cover urgent needs.

4. Instalment Loans from Regulated Lenders

These come with clear terms and better consumer protection.

5. Budgeting and Financial Planning Services

Professional advice can sometimes prevent the need for short-term borrowing altogether.

Best Practices for Safe Borrowing

To protect yourself financially, follow these guidelines:

- Borrow only what you truly need.

- Compare multiple loan options before making a decision.

- Calculate whether you can comfortably manage the repayment schedule.

- Keep copies of all agreements and correspondence.

- Prioritise lenders with strong reputations and transparent terms.

Conclusion

Chirpy check loans have become a widely searched phrase due to the growing demand for quick and convenient lending solutions. Yet the term itself does not refer to a well-established or widely recognised financial institution, making it crucial for borrowers to proceed with caution. While such loans may offer quick relief in urgent situations, they come with notable risks, including high interest rates and potential exposure to unregulated providers.

By understanding how chirpy check loans work, recognising red flags, verifying lender legitimacy, and exploring safer alternatives, consumers can make informed borrowing decisions that protect their financial wellbeing. Responsible borrowing, thorough research, and careful evaluation remain essential—especially when dealing with unfamiliar loan terms or emerging financial brands.